Does Bitcoin really lag Global Liquidity?

Is it a false narrative we have been told?

Aloha friends,

In this piece, I’ve looked at Bitcoin and Global Liquidity, as there are many voices out there talking about a lag between Bitcoin and liquidity.

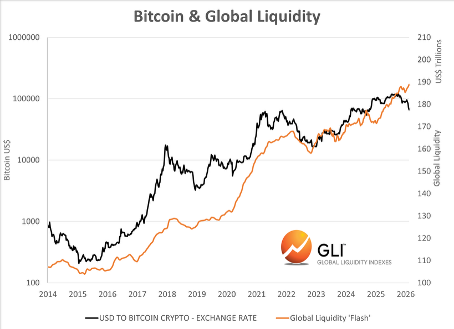

Last week, Global Liquidity rose to a record $188 trillion! This was mainly driven by another PBoC injection ahead of the Chinese New Year and the further weakness of the USD. So, if the “lagging” narrative is correct, we should see a rally within the next few months (according to Raoul Pal, who states in Global Macro Investor that Global Liquidity explains 90% of Bitcoin’s price action). But is this really the case?

Let’s take a look at the data for a deeper dive.

Disclaimer: Views expressed are the author’s personal views and should not be relied upon as investment advice.

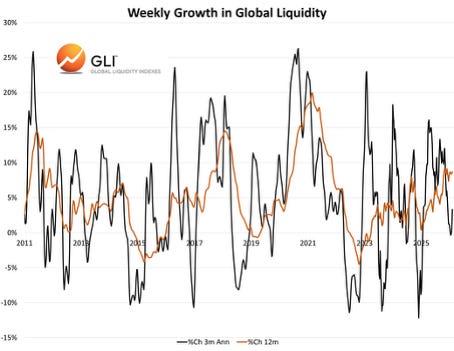

Currently, we see the 3-month annualized growth rate at 3.6%, while the annual growth rate sits at 8.7% with Global Liquidity at an all-time high (ATH).

Looking at this narrative or data, one could easily draw this conclusion. Nevertheless, if we look at what happened in previous cycles, Global Liquidity continued to increase even after Bitcoin peaked.

This suggests that what we’ve been told might not reflect reality. One could ask the question: Is Bitcoin perhaps not lagging Global Liquidity, but actually leading it?

Think about it. Markets in general are forward-looking (as seen when earnings reports are released, etc.). Since Bitcoin can be traded 24/7, all information on a global scale is immediately reflected in the price. Why would it lag? From my perspective, there is a valid chance that Bitcoin acts as a front-runner for an upcoming drainage of liquidity.

But maybe that’s too simple. When looking at the bear market, Global Liquidity seems to lead again. Why? Probably because in this environment, markets are waiting for clear signals from central banks and the government.

If what I’ve written above is true, we should see a drop in Global Liquidity soon. You might remember: in the previous cycle, the Fed’s rapid rate hikes, as a response to pandemic-induced inflation, caused a liquidity squeeze.

What could it be this time? With Kevin Warsh recently announced as the new Fed Chair, we’re seeing some interesting signals. He is known for being more hawkish:

· He clearly states a willingness to reduce the balance sheet, which is usually not a “sweet spot” for risk-on assets.

· He wants to curb government spending.

· He may not favor Quantitative Easing as much as previous Fed chairs did during crises.

I am aware he also favors cutting interest rates quickly rather than slowly; however, the current economic setup does not seem very stable and might result in a short-term pain scenario. Since I believe we are currently in a crypto bear market, all of this would only confirm this thesis.

Final Thoughts

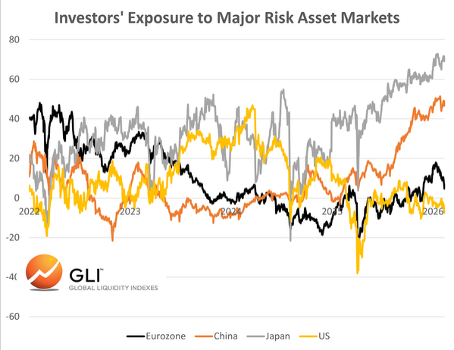

As shown above, Bitcoin led Global Liquidity at previous cycle tops. And today? We see a potential shift in fiscal policy with the new Fed Chair. This will likely not have a positive impact on risk-on assets during this transition phase. Markets in the US and Europe are already “pricing this in,” with asset allocation strategies shifting to “risk-off” mode, and the Eurozone and UK following suit. Outliers are still Korea and China.

Portfolio Allocation

Based on the current setup, I remain in favor of staying patient and not leaning into “risk-on” mode just yet. The combination of a potential liquidity drainage and a shifting policy regime suggests that a defensive posture is the wiser choice for now.

That’s it for today - I hope I could deliver some valuable insights.

Maloha

Stay Humble. Stay Curious. Enjoy the Journey.

Disclaimer: Views expressed are the author’s personal views and should not be relied upon as investment advice.