The Boring Phase

Health Check: Decoding the Silence

Aloha friends,

We are entering a phase where Bitcoin seems not to be of interest for many. From mainstream media to X, forums, and Discord, the spotlight has shifted elsewhere. Global attention is currently fixated on the conflict in Iran, the latest Epstein revelations, and surging oil prices.

So, is Bitcoin dead (for now)? Hardly. We are simply entering the boring phase. The quiet period where focused observation pays off. Fun fact: Bitcoin has been declared dead 471 times to date (Source: bitcoindeaths.com). And yet, here we are. Today, I am checking the health of the network.

Disclaimer: Views expressed are the author’s personal views and should not be relied upon as investment advice.

Network Vitality: The Hash Rate

The Hash Rate is perhaps the most critical metric for Bitcoin’s health. An increasing rate means the network is more expensive to attack and signals long-term capital commitment. Mining is a capital-intensive business; no one invests billions into hardware and infrastructure without deep confidence in the network's longevity.

Currently, the hash rate is down about 7% from its peak, but it has grown nearly 4x since early 2023. However, a challenge is coming up for miners. The network currently generates roughly $30M in daily block reward payouts (Source: Bitinfocharts). With the block rewards decreasing each halving every four years, miners face a revenue squeeze if BTC price appreciation or transaction fees (currently only ~0.6% of revenue) don't compensate for the reduction.

This week, we also reached a milestone: the 20 millionth Bitcoin was minted, meaning only one million coins remain to be discovered (95.2% are already in circulation).

What does this show us?

The hash rate is increasing, but the block rewards are not, which means that miners need to find ways to increase their market share in order to increase their revenue potential (or they will not be cashflow positive anymore). For this, they would need capital and access to cheap energy to do so. At the end, this will favour larger miners and the decentralisation of the network will decrease.

Network Usage

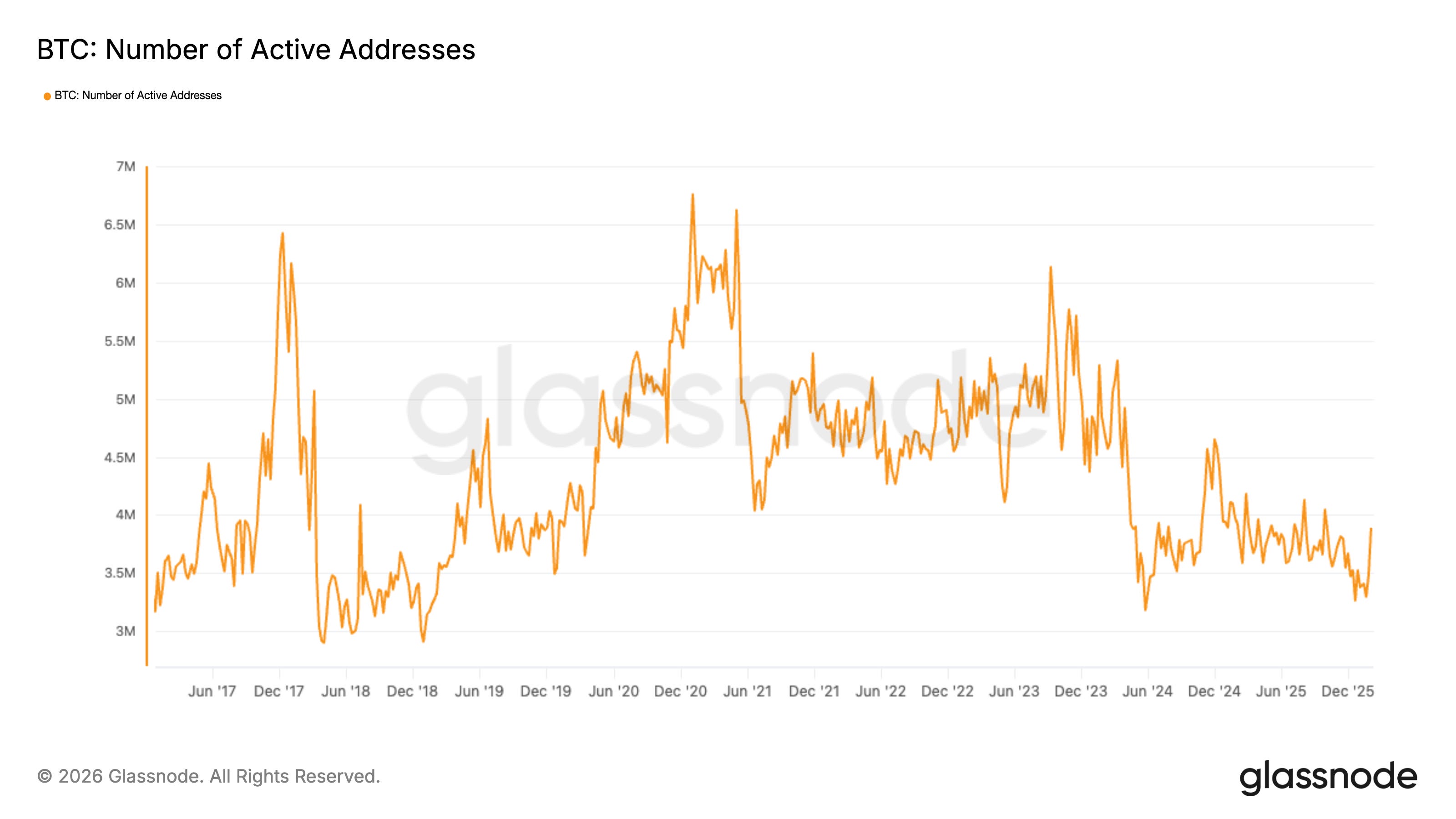

On-chain data shows that active addresses are hovering near levels seen in 2017 and 2018. Why hasn’t this increased?

The answer lies in how we use Bitcoin today. Most participants interact through centralized exchanges, ETFs, custodians, or "wrapped" BTC. These layers handle the activity off-chain, meaning they don't generate new on-chain addresses.

As Bitcoin is also not being used for payments (as some people thought it could be), there is no increasing on-chain usage from this side.

The potential risk we have here is, if the active addresses continue to go down while the transactions fees keep as low as currently, miners could get under pressure at some point. Of course only if the Bitcoin price is not keep going up over time (which is however my thesis).

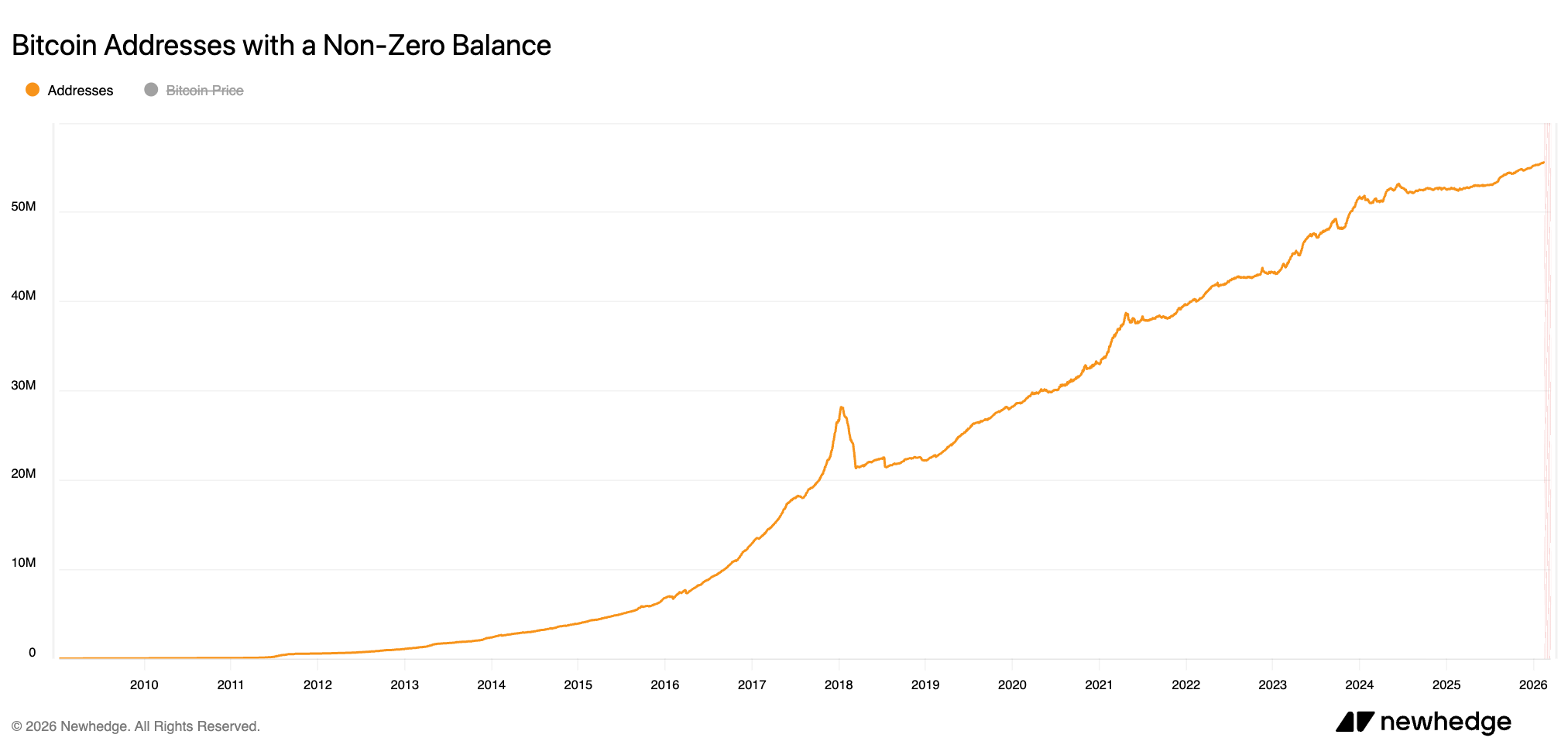

Looking at the addresses in general however, we see still a steady increase - they doubled within the last 6 years. So even with less active addresses, one could anticipate, more people buy and hold for a longer period and see a case for the digital gold concept.

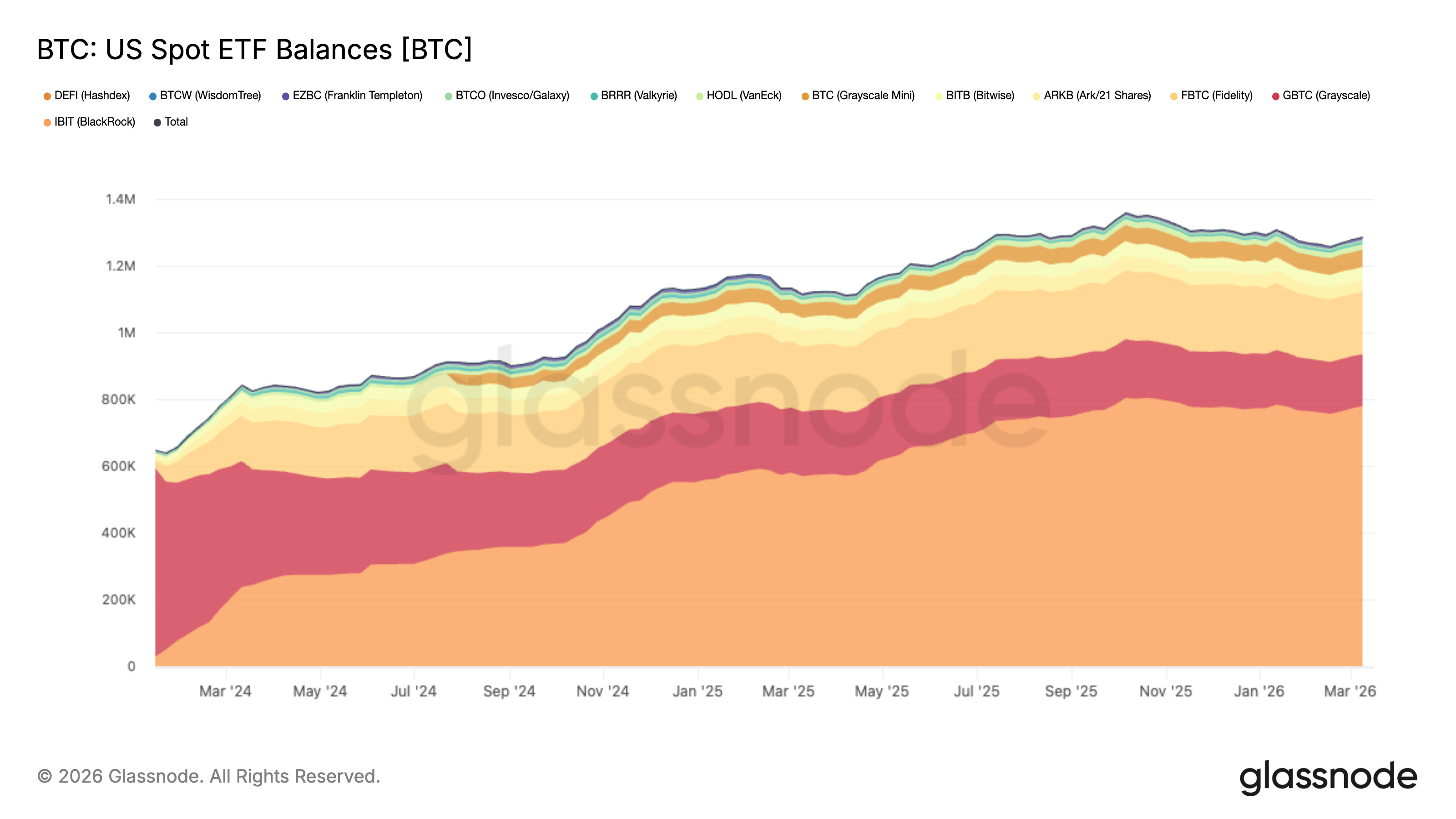

Institutional Adoption

As mentioned earlier, we had the most successful ETF launch with Bitcoin. This reflects in currently 1.28m Bitcoin being hold by ETFs. That is 6.1% of the total supply. Also the fact, the even if we had a large pullback of the BTC price, the ETF holdings are only down around 9% from its all time high - this in fact, is a very positive signal.

So according to this data, ETF holders seem to have strong hands and these investors are more into long term holding rather than looking for a quick Dollar.

Next to the ETFs we also have a lot of holdings by other entities and treasury companies (Source: BitBo):

Countries: 518.526 BTC ($37.06 Billion)

Public Companies: 1.109.520 BTC ($79.29 Billion)

Private Companies: 431.260 BTC ($30.82 Billion)

BTC Mining Companies: 126.786 BTC ($9.06 Billion)

Defi: 267.236 BTC ($19.10 Billion)

Including ETFs, approximately 17% of the total supply is now in institutional or state hands. Ask yourself: would these entities deploy billions into an asset they believe is going to zero?

Final Thoughts

Bitcoin remains a risk-on asset, but the risk/reward profile is shifting. I believe Bitcoin is actually becoming less risky to hold over time. It has 100% uptime, has never been hacked, and is now integrated into the offerings of almost every major global bank. The U.S. government has even established a Strategic Bitcoin Reserve.

While influencers (or whatever you want to call them) talk about a return to $1.000 or claim it’s a Ponzi scheme, the data tells a different story:

Hash rate is up 6x over the last few years.

Institutional integration is complete (ETFs, custodians).

Bitcoin maintains its dominance as the #1 crypto asset.

Yet, only about 2% of the global population owns it. To me, that sounds like a very asymmetric opportunity.

Portfolio Management

No changes in my portfolio this week. I used the recent supply area retest to increase my short positions. Since we didn't fully reach my expected ceiling, the relief rally may not be entirely over: the $74k–$80k range remains a possibility.

However, on a macro scale, I am still looking for lower prices. Rising oil prices and a weakening S&P 500 at the end of the week could create further headwinds for Bitcoin. I’m staying patient (as you know by now).

That’s it for today - I hope I could deliver some valuable insights.

Maloha

Stay Humble. Stay Curious. Enjoy the Journey.

Disclaimer: Views expressed are the author’s personal views and should not be relied upon as investment advice.