The Liquidity Cliff

Why the FED's $172B Liquidity Buffer is Fading While Bitcoin Stalls at the Squeeze

Aloha friends,

The week ended up being flat, and in terms of price action, we didn’t see much movement in the crypto space. Interestingly, Michael Saylor did not buy last week. This raises a pressing question: if Saylor isn’t buying, are we losing the fuel for any further upside?

Meanwhile, it was another record-breaking week for the NASDAQ and S&P 500, fueled by staggering earnings from AI-heavy businesses. Google, in particular, posted record numbers, leading to a 9% stock surge following their financial reportings. So, where are we heading now? While the stock market celebrates, Bitcoin feels increasingly heavy. Let’s look under the hood to see why this divergence is growing.

Disclaimer: Views expressed are the author’s personal views and should not be relied upon as investment advice.

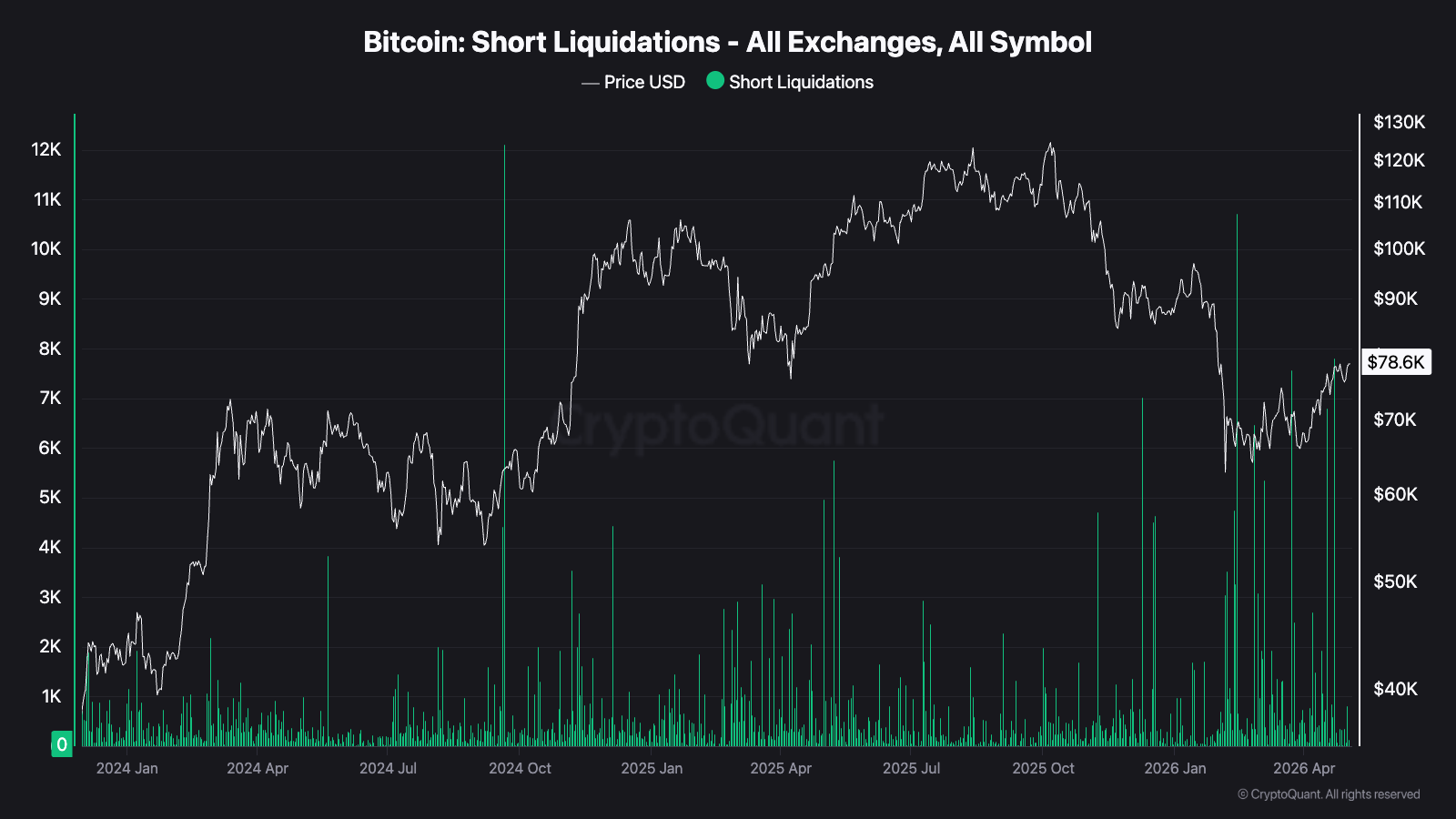

Bitcoin: A Squeeze Without Follow-Through

With no support from MicroStrategy’s purchases this week, Bitcoin has remained largely stagnant. This positioning resulted in the 3rd most short liquidations over a 1-week period across the last two bear markets.

Normally, this would be a bullish trigger. Short liquidations often lead to short squeezes, where prices rise reflexively as exchanges are forced to buy back positions.

Despite this squeeze and the fact that MicroStrategy deployed $2.3b into BTC over the previous weeks, price still hasn’t been able to push into the $80k – $84k resistance range.

Volume: Spot volume remains at exceptionally low levels

ETF Flows: Inflows have failed to ramp up and remain muted compared to previous cycles

Given that the Fear & Greed Index is at its highest level in three months, it is alarming that BTC hasn’t broken higher. The lack of “follow-on” bulls suggests this rally is on borrowed time. If you believe, as I do, that we have not yet hit the macro low, this derivatives-driven action is a bearish signal, not a bullish one.

In terms of Strategy, I am closely observing their actions over the next weeks and what impact they keep having on the market.

Stocks: Climbing the Worry Wall

Why are stocks still surging while crypto stalls? The setup for traditional markets is a paradox of high risks and high earnings.

The Macro Backdrop:

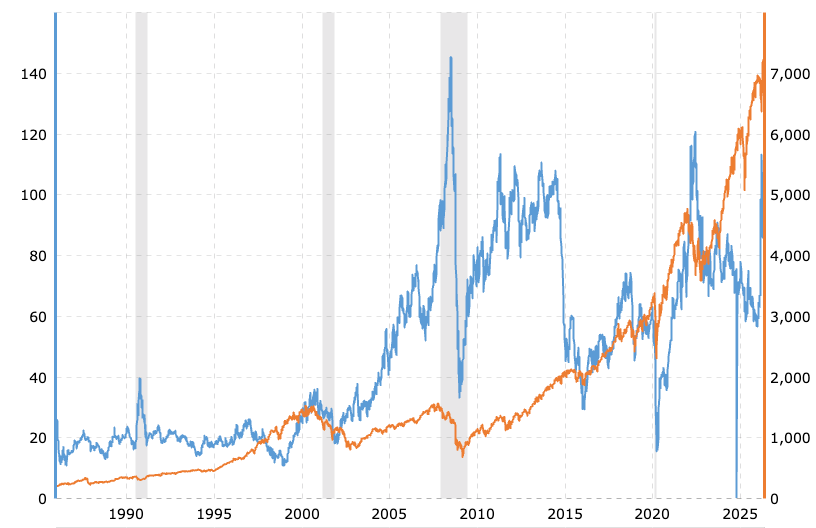

Energy Crisis: WTI is hovering near $102, with Brent between $108–$118. Driven by the ongoing Iran conflict and risks in the Strait of Hormuz, prices are up 75% YoY

Sticky Inflation: The March CPI came in at 3.3% YoY, driven almost entirely by energy (+12.5%)

FED Hardline: Markets are now pricing in practically zero rate cuts for 2026. The FED is waiting for energy-driven effects to cool before even considering a pivot

Source: MacroTrends - Crude OIL vs S&P 500

Why the New Highs in S&P and NASDAQ?

The Earnings Power is currently winning the tug-of-war against macro headwinds. Q1 results showed a blended earnings growth of ca. 27%. Furthermore, the US is now a net exporter of energy, making the S&P 500 more resilient to oil shocks than in previous decades. We are seeing a rotation into value and energy, while Big Tech continues to ride the AI Capex wave. However, it will be interesting how earning in Q2 & Q3 will end up, when the reality of war impacts might hit the earnings. Additionally, looking at the performance of the S&P 500 - the rapid decrease of oil value actually brought down the stock market and not it’s increase. Something to take a look at.

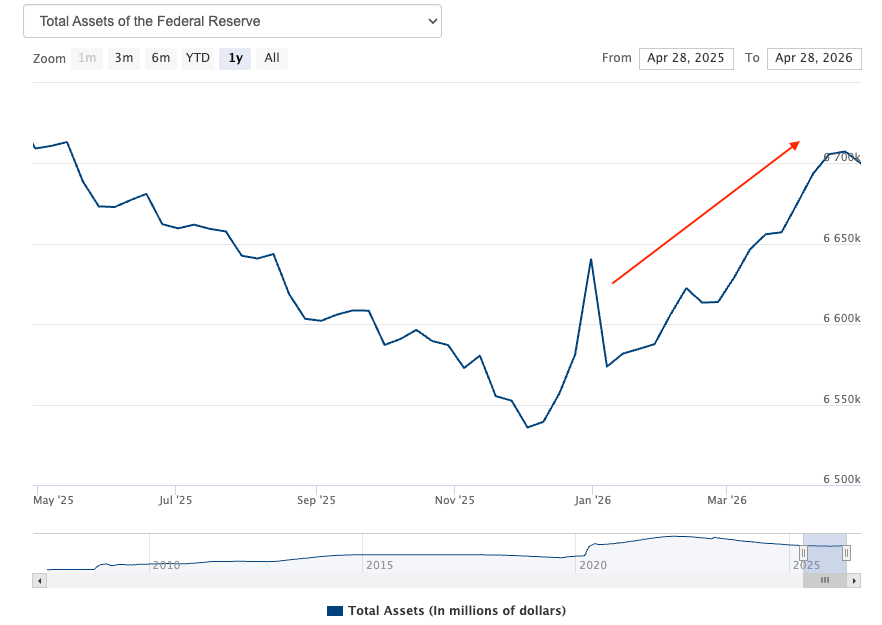

The RMP Cliff: A Temporary Liquidity Buffer?

While Global Liquidity (according to GLI) appears to be rolling over, the FED has added $172b to its balance sheet since December. This was driven by the “RMP purchases” (Reserve Management Purchases) program.

This program boosted banking-sector liquidity and dampened bond volatility, effectively pushing the markets. The Nasdaq is up 20% over the last month alone. However, the FED guided that these RMP purchases were temporary, intended to offset seasonal fluctuations like tax day.

Now that the April 15th tax deadline has passed, this liquidity buffer is expected to be significantly reduced. We are likely approaching a liquidity cliff just as Kevin Warsh prepares to take office. If this temporary support is removed, the “Worry Wall” might finally become too steep to climb.

Portfolio Management

My thesis remains unchanged: the structural risk points to the downside. We are nearly seven months into this bear market, and I still anticipate one more significant drawdown for BTC to find its true macro floor.

While I am keeping my dry powder ready, I am starting to look closely at specific Altcoins. In the 2022 bear market, assets like ETH bottomed before Bitcoin.

Many Alts are already deeply oversold. While they may not increase in absolute dollar value immediately, they may begin to outperform BTC on a relative basis.

I expect further weakness for BTC in the short term, and I believe BTC dominance will ultimately drop from current levels as the rotation begins.

That’s it for today - I hope I could deliver some valuable insights.

Maloha

Stay Humble. Stay Curious. Enjoy the Journey.

Disclaimer: Views expressed are the author’s personal views and should not be relied upon as investment advice.